In this letter, I will take a moment to look back at some of the important developments in our portfolio over the last year, then I will provide a business update in which I discuss some changes I am making to Highwood and the way I communicate with you. Finally, I will provide the usual snapshot-in-time valuation of the portfolio and an update on each of our holdings.

Review of 2023

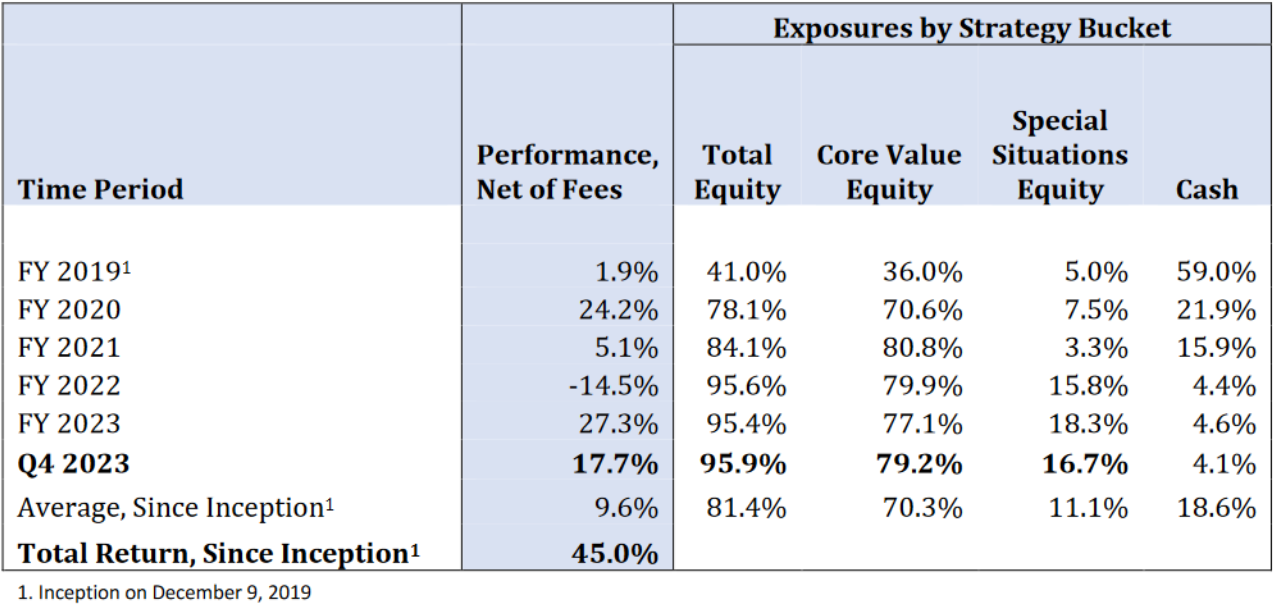

Highwood was up 27.3% after fees in 20232. The result was driven by strong performance from Borr Drilling (+48% in 2023), Ryanair (+52%), Burford Capital (+91%) and Hotel Chocolat (+120%) with limited impact from mark to market losses on other holdings in the year.

Historically, I have counselled for a cautious approach to drawing conclusions on the investment merit of our holdings from short term price movements driven by the vicissitudes of buyers and sellers of their shares. I continue to advocate that view as both rational and profitable over the long term.

The share price developments in 2023 for Borr Drilling, Ryanair and Burford Capital were driven largely by fundamental developments in these businesses. I am pleased these developments were consistent with my investment thesis for each investment. Our shares in Borr Drilling appreciated on the back of increased day rates for the company’s rigs, profit growth of 140% year over year and progress on refinancing the business, which is now complete. Ryanair’s profits were up 60% in the year driven by market share gains across Europe, the result of an industry leading cost position and counter-cyclical investments made during the Covid pandemic. Shares in Burford appreciated in the year as a result of positive developments in the company’s YPF legal matter vs Argentina and growth in realisations from the portfolio excluding YPF. While it was outside my circle of competence to have a strong view on the outcome of the YPF case, it was clear to me that the price of the shares at the time of our investment attributed little or no value for this option after accounting for the value of the core business excluding YPF.

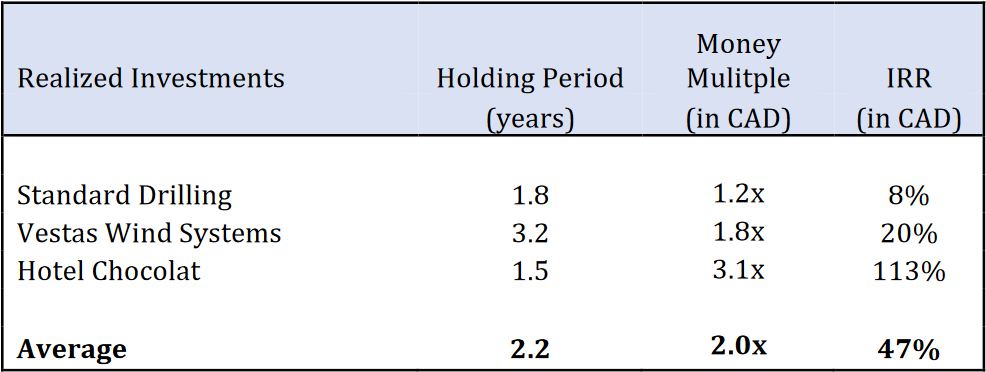

Turning to realized gains, we made 3.1x money and a 113% IRR3 on our investment in Hotel Chocolat during the year. In mid November, Mars Inc, the global chocolate and pet food business offered to acquire Hotel Chocolat for £3.75 per share in cash, which was a 170% premium to the closing price prior to the deal. We paid £1.33/share for our holding in the third quarter of 2022 on the basis that this was a high- quality branded business, well managed and substantially undervalued. A 170% premium from a rational, well-regarded competitor such as Mars reflects how wrong the public equity market was in its assessment of the value of this business. While this is gratifying, I also believe there was a multi-year path ahead for the company to be worth considerably more than £3.75 per share, as indicated by the terms of the deal.

The offer from Mars included a Partial Share Alternative (PSA) which allowed up to 30% of the shares to be rolled into the privatized Hotel Chocolat with Mars retaining a call option on those shares at pre- determined prices depending on the EBITDA of the company over the next five years. The terms of this PSA give a good indication of what Mars and the board of Hotel Chocolat believe is a realistic range of outcomes for the profits from the stand-alone business over the next 5 years. If Hotel Chocolat performs well over the next 5 years and EBITDA exceeds £80mn, those rollover shares will be worth c. £11.00 each4, and the purchase price for the 70% of shares acquired in January 2024 for £3.75 will end up looking like a bargain. In a less optimistic scenario, if EBITDA ends up at £60mn or less, Mars has agreed to acquire the rollover shares at a weighted average price of c.£4.40, or a 17% premium to the offer price of £3.75/share.

This is an attractive risk-reward, and I reviewed the option of rolling our shares into the deal. However, the PSA was constructed to permit the founders and 57% owners of the company to roll the majority of their shares into the deal and limit the participation from minority shareholders. The terms of the PSA were carefully crafted to establish it more as an equity compensation program for the founders who will continue to manage the business.

I point this aspect of the deal out as I think it shows that the board of Hotel Chocolat and Mars see a clear path to delivering substantially higher profits in the future, and more than £3.75/share in value. To me, this underlines the point above that the public equity market had substantially mispriced this business. It is a fine example of why I believe a fundamental value-oriented strategy with a long-term approach focused on public markets is rational, and if well executed, capable of compounding our collective capital at attractive rates.

I am now focused on re-deploying the proceeds from Hotel Chocolat shares into situations with similar characteristics and, we hope, similar results. I will have more to say about this in upcoming letters.

Business Update

That brings me to a look forward to the future. I am making two changes to Highwood which I hope will be constructive to the rate of long-term compounding for our capital. First, I will be consolidating as many of your managed accounts as possible onto a single platform. I have had enough time to assess our various service providers and am confident that one is clearly better than the other, particularly when it comes to trading costs and interest rates received on overnight cash balances. Consolidating accounts onto one platform will also reduce the operational complexity of managing them. I will be contacting each of you to have this conversation and am happy to discuss the rationale in more depth.

Secondly, I will go from writing four letters per year to two, one in January and one in July. Of course, I will continue to provide you with quarterly statements, performance reports and am free to have conversations with you whenever you would like. I have now written sixteen quarterly letters to investors, which I believe provides a good overview of my mission and strategy with a number of examples. They are posted here for your reference. Four years on, Highwood has made fourteen investments and exited three. Our strategy is inherently low turnover, and semi-annual letters aligns more closely with the rhythm of important developments in the portfolio. Finally, while I value the frequency with which I communicate the investment thesis and developments for each holding, I am aware that it comes with the potential cost of optimum impartiality. This is the consistency and commitment bias that the late, great Charlie Munger referred to as the fourth cause of human misjudgement5. Highwood was founded on four core values, one of which is constant self-improvement (as an investor), and this change feels consistent with that value.

Finally, I will include the table below as an appendix going forward. It shows the result of realized investments since inception. I think this is helpful additional disclosure – it indicates how Highwood has performed excluding the mark-to-market price of our holdings, which by definition I believe undervalues those holdings.

Highwood has grown assets under management by 52% year over year through a combination of performance and new clients. I am grateful for your trust and look forward to diligently pursuing the mission of compounding your capital alongside my own family’s.

Portfolio Updates

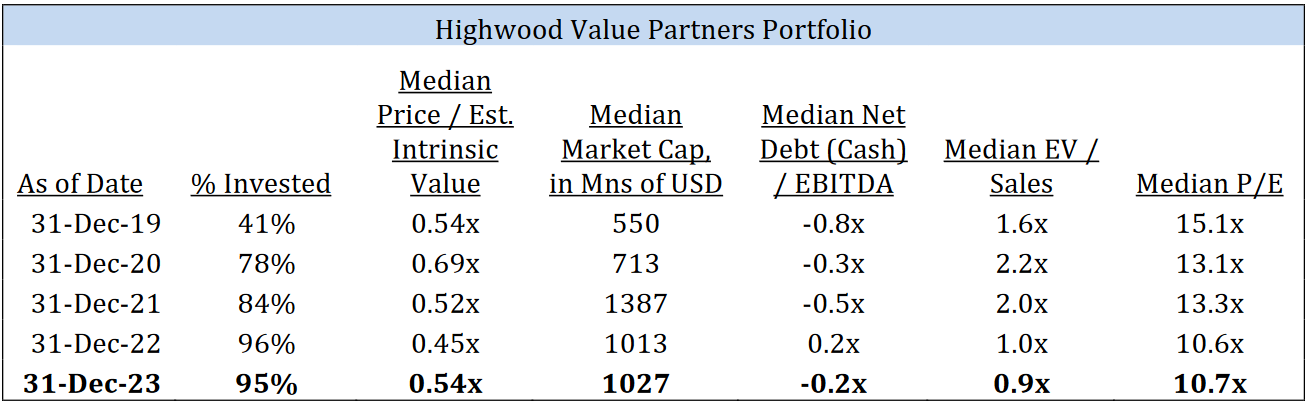

Below is the usual table which summarizes key statistics on the portfolio as of December 31st. I have excluded Hotel Chocolat from the valuation statistics – as of December 31st it was effectively a cash alternative. The portfolio is priced at 54 cents on the dollar of my estimate of intrinsic value, the median P/E is 10.7x and portfolio companies on average have net cash balance sheets (Net Cash/EBITDA of 0.2x).

Below are the updates on our portfolio holdings in order of their contribution during the year excluding Hotel Chocolat.

Burford Capital – Core Value

Burford Capital is our UK listed global market leader in litigation finance. The company makes money by funding select commercial litigation claims in exchange for a share of the proceeds if successful and by generating fees on third party capital as the largest asset manager in this attractive niche asset class. It has been an eventful year for Burford. The YPF matter has garnered most of the attention, and with that much speculation about whether Argentina can pay, will pay, and if so, over what time period. The successful summary judgement in March and the election of Javier Milei in December has increased the probability of a successful result, but there remains a number of hurdles before shareholders of Burford can count their chickens. While attention has been focused the YPF case, it is worth remembering a couple of important points. First, the YPF case is one of c.225 cases Burford has on its balance sheet at present. All of these matters meet the same underwriting thresholds which resulted in Burford funding the YPF case. Second, Burford continues to underwrite new cases every year, and each year with the benefit of more experience, a larger database of concluded matters and greater balance sheet scale. So, in a sense, the question I ask is not just ‘what will Burford get from the YPF matter’, but also ‘what is the likelihood of additional matters of a similar significance in Burford’s future?’. My checks with industry players suggest that Burford is increasingly the partner of choice for law firms and large corporates that may be the plaintiffs in such cases. So, let’s invert this question and ask, ‘what are the chances that Burford does not end up funding similarly valuable cases in the future?’. I believe the odds are on our side, and in the meantime we own the equity today at a price that does not discount such a favourable scenario.

Ryanair – Core Value

Ryanair is our large cap, Irish listed discount airline that is able to price its fares at a 30% discount to the costs of competing airlines and still earn a low twenties return on capital in a normalised environment6. Ryanair continues to execute well. Profits were up 60% over the 6 months to September 30th, the business’ cost advantage has widened, the balance sheet is back to a net cash position and the company re-instated a dividend. Industry wide short haul air travel in Europe remains c.7% below pre Covid levels, yet traffic on Ryanair is 23% above it’s pre-Covid level. Ryanair has taken this market share profitably. The company is now on track to deliver profit per passenger of €10 on average fares of c.€55 per passenger. Meanwhile, the incumbent national airlines are charging fares 3-4x Ryanair’s and making lower profits per passenger. The strength of Ryanair’s balance sheet is now opening up attractive options for capital allocation. Our owner-operator management team are well versed in the art of share buybacks as a means of increasing per share value. With the shares at 11x earnings and a net cash balance sheet, the potential value creation from retiring shares is both attractive and actionable.

I think it is worth pointing out that this time last year, the outlook for the European consumer was pessimistic at best. Yet here we are one year later and Ryanair has powered through with profits 60% higher year on year. Part of that is the result of a softer landing for the consumer, but by far the majority of this result is directly attributable to Ryanair’s superior cost position and consequent market share gains. Yes, we are owners of an airline, but the economic productivity of our airline is rather unique, which goes a long way to insulating us from the changing fortunes of the airline industry.

Borr Drilling – Special Situation

Borr Drilling is our mid-cap, Norwegian listed owner of shallow water drilling rigs and is one of two special situations investments for Highwood. The summary thesis on our investment in Borr is available here. The business continues to execute well and is making progress against that thesis which has resulted in an unrealized gain of c.2.8x on the position. During the quarter, the company completed the refinancing of its debt structure, which pushes out the significant maturities from 2025 to 2028 and 2030 at a cost of c.$20mn in incremental interest payments per annum. The new capital structure permits management more latitude on capital allocation and promptly after the refinancing the board re-instated a dividend and then, later in the quarter, authorized a share buyback equivalent to 5% of the market cap. Borr will have very limited capital requirements going forward (c.5-7% of EBITDA annually) and is moving toward de- levering and returning capital to shareholders as rig rates continue to improve. This part of the thesis also looks good, but I remain very aware that things can change quickly in this industry. Leading edge day rates continued to move up in the quarter (most recent deal at $170,000/day), which is driving strong results. Year to date, Borr’s revenue is up 87% and EBITDA is up 139%. Run rate EBITDA is now c.$430mn and this continues to grow as old contracts expire and rigs are re-contracted at today’s rates. On the basis of 2024 estimates, Borr is trading at 5.5x EBITDA and a 20% equity free cash flow yield. The board was also strengthened during the quarter with the addition of Jeff Currie, who was previously the head of commodities research at Goldman Sachs where he had a well regarded 27yr long career.

Protector Forsikring – Core Value

Protector is our mid-cap, Norwegian P&C insurer with a cost advantage in underwriting which feeds a large and growing float. My thesis on Protector is playing out well and we have achieved a (partially realized) 4 year 48% IRR on this investment since our purchase. In total, we have received dividends equivalent to 27% of our initial cost to acquire the shares. Protector continues to deliver strong results. In the first nine months of the year, net income is up 9% driven by strong growth in insurance underwriting partly offset by lower income from the investment portfolio. On the insurance side of the business, Protector grew premiums at 34% year over year at an 89% combined ratio. This strong growth is feeding a growing investment portfolio and float, the income from which goes to shareholders. As of quarter end, Protector had a bond portfolio of 15bn NOK invested at a 5.9% yield, which is generating after tax income of 9 NOK per share, or a 4.6% yield on the current share price.

Alimak – Core Value

Alimak is our mid-cap, Swedish industrial business which operates an attractive installed base business model. The business reported solid Q3 results during the quarter. Profits were up 7% organically and cash flow improved meaningfully such that net debt is now back below 2.5x EBITDA. Margins continue to track toward management’s goals of at least 18%. Alimak is a global business with dominant market share in the US (north of 50% in Industrial elevators) and a management team that is increasingly proving it is able to execute well operationally and allocate excess free cash flow at attractive incremental returns. The public equity market is pricing this business at 12x earnings which is well below where a negotiated private market sale would take place.

GetBusy PLC – Core Value

GetBusy is our small-cap, UK listed productivity software business with a strong position in the tax and accountancy vertical, good economics and a net cash balance sheet. There was little new news on this holding in the quarter. Similar to the situation with Hotel Chocolat, I believe the public equity market is valuing this business at a significant discount to what a rational acquiror in the private market would pay for the asset. GetBusy is valued in the public market at 1.3x revenue. Contrast this with the 7x revenue the likes of Thomson Reuters, Wolters Kluwer and IRIS have paid to acquire similar assets in the tax and accountancy vertical over the past three years. Moreover, we are partnered with a management team that is incentivized to make a cash distribution to us as shareholders of between 2x and 5x the current market cap of the company7 – something that would only be possible through a sale of GetBusy or one of its two core assets. One risk we are taking in such a fast-changing industry is technological obsolescence risk, ie. that GetBusy’s products become less relevant over time. Not only does the evidence to date suggests customers are voting with their feet (revenue is growing low double digits with stable gross margins), but if I am correct, we are warehousing this risk over a relatively shorter time period.

JZ Capital Partners – Special Situation

JZ Capital is our small cap, UK listed closed-end private equity fund in liquidation. Our shares in the fund were marked up 22% in the quarter driven by two positive developments. JZCP sold the fund’s interest in Felix Storch for $62.5mn, which was a 30% premium to NAV. Felix Storch is a supplier of specialty medical refrigerators and cooking appliances and was the fund’s single largest remaining asset. Following this, JZCP repaid the senior credit facility, which was the last remaining debt obligation of the fund. At quarter end, the fund NAV is composed of $197mn of Private Equity assets and $120mn of cash. The publicly traded shares in the fund now trade at a 38% discount to NAV, which is the narrowest discount it has traded at since we acquired our shares. Against this, the excess cash balance in the fund now opens up the option for JZCP to tender for shares in the public market as a means of returning capital. This would be an intelligent use of capital and I have recommended this option to the manager of the fund. Our downside from the current share price is well covered even if the remaining assets are sold at a large discount to NAV and the potential for an accretive return of capital through a tender offer could increase our upside substantially.

Sto SE – Core Value

Sto is our German listed, family run international manufacturer of building coatings with a dominant market position in external wall insulation in Europe. You can read the investment thesis here. Sto reported Q3 results during the quarter and I had a call with the outgoing CFO, Rolf Wohrle. STO is exposed to construction activity in Europe, which has declined this year. However, Sto increased prices and as cost inflation has eased, they have seen margins improve such that the business is likely to keep profits stable this year despite revenue down low single digits. The business has a strong balance sheet (20% of the market cap in cash) and has consistently delivered mid teens returns on capital and mid single digit growth annually (over decades). We have a strong margin of safety based on the business quality and the public market valuation for the shares of 0.4x revenue and 8x earnings. If the EU is serious about reaching their sustainability targets, Sto’s target market (as measured in square meters of product applied) could expand by 3-4x. This would of course be a fantastic outcome and I believe we own a low risk, high return business with an attractive yield while we wait.

Motorpoint Group PLC – Core Value

Motorpoint is our UK listed small cap and the largest independent used car retailer in the UK. The business is run by Mark Carpenter, who has the vast majority of his net worth invested in the shares of the company. Motorpoint has the lowest costs in the industry which allows it to consistently offer lower prices on like for like product in an industry with a high degree of price comparability. This has resulted in steady market share gains in its segment at attractive returns on capital. We acquired our shares in Q1 of 2023 and the summary thesis on the investment is available here. During the quarter, I had another call with Mark and came away reminded of Winston Churchill’s old saying, ‘never let a good crisis go to waste’. Motorpoint makes a small profit on each car it sells, and hence the P/L is a function of profit per unit times number of units sold. Units sold in Motorpoint’s addressable market are down 40% from pre-Covid levels, and management is certainly making use of the challenging operating environment. They are laser focused on the engine of competitive advantage in this business, which is lowering costs and turning inventory faster.

Over the past year, they have taken 16% out of corporate costs and increased inventory turn by 10%. I continue to believe Motorpoint will emerge as a materially larger and more profitable business as the supply into the used car market normalizes. In the meantime, I am acutely aware of the economic sensitivity of the P/L of this business and the position is sized accordingly. We own our share of this business at 6x average pre-Covid earnings and a low single digit multiple of my estimate of normalised free cash flow.

Naked Wines – Core Value

Naked Wines is our UK listed online direct-to-consumer subscription wine business. The company has struggled mightily in the post Covid period. Some of this has been the result of weaker fundamentals, but the majority of it has been the result of self-inflicted wounds from a management team led by Nick Devlin and Shawn Tabak that made too large a bet on the growth of the US business coming out of the pandemic. As I said in my last letter, these mistakes fall into the category of management not thinking like owners of the business: they swung for the fences rather than budgeting conservatively. I am pleased that we now have a more aligned management team in place. Nick and Shawn have both left Naked Wines and Rowan Gormley, the founder and a significant shareholder himself, has returned as executive Chairman. James Crawford has returned to the CFO post after running the UK business. The company also recruited a new head of the UK business, Rodrigo Maza, during the quarter.

The business is facing stiff headwinds, but management are doing the right things in my opinion. Year to date, revenue is down 15% and management have taken costs out of the business to remain profitable. Net Assets of the company (ie after all balance sheet liabilities) is 2.1x the market capitalization, which is to say the equity is trading at a discount to its balance sheet liquidation value. The largest asset on the balance sheet is £161mn of inventory, which was acquired as part of the previous management team’s bet on growth. The new management team are moving toward monetizing the excess inventory, which I expect will result in a cash inflow to the company of £40-50mn over the next 15 months, a figure which is also greater than the current market cap. So, we own equity here at a discount to the liquidation value of the business, I believe the business will see cash inflows in excess of the current market cap over a short period of time and we are now partnered with a management team who have significant skin in the game. Rowan Gormley and a number of the board members bought more shares in the open market during the quarter which I think signifies their confidence.

As always, I thank you for your trust and welcome your questions and comments.

Sincerely,

Desmond Kingsford

1 MSCI Europe (in CAD) and TSX respectively.

2 In Canadian dollars.

3 Both figures in Canadian dollars.

4 Depending on balance sheet debt at December 31, 2028, which I expect to be nil in this scenario.

5 Please see a brief explanation in his own words here.

6 Ryanair’s return on capital in the ten years prior to the COVID-19 pandemic was 22.4%.

7 See my Q1 2023 letter in which I discuss managements Cash Distribution Incentive plan here.

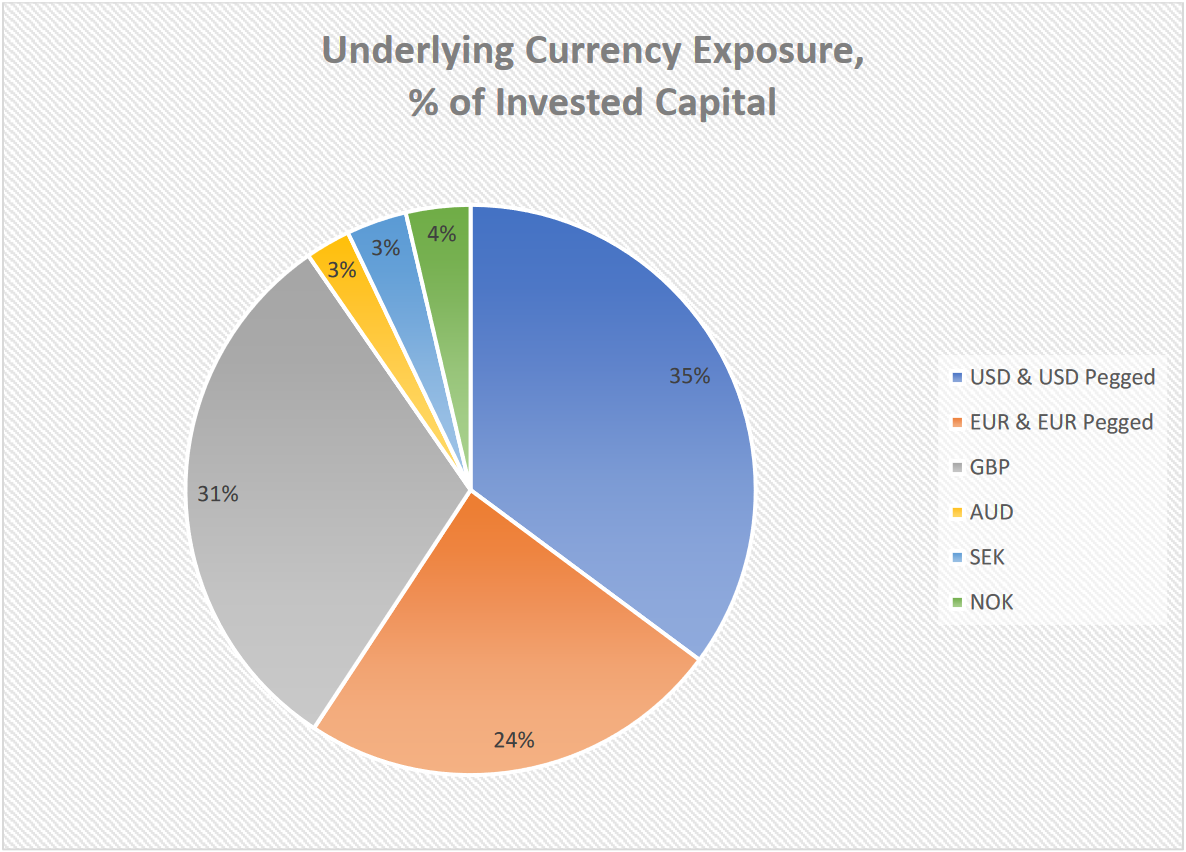

Appendix 1: Underlying Currency Exposure Split

This is not a breakdown of the listing currency of our holdings. It is the split of the currencies our portfolio companies earn their revenues in. As such, it is the underlying exposure to currencies you have through your partial ownership of these businesses. As investors can choose whether to have their account in USD or CAD and hence their cash balance may be in either USD or CAD, I have expressed the currency exposure as a percent of invested capital.

Disclaimer:

This letter (“Letter”) provides a general description of Highwood Value Partners, Inc. (the “Firm”). The Firm is registered with the British Columbia Securities Commission, the Alberta Securities Commission and the Ontario Securities Commission (the “Commissions”) as a portfolio manager under National instrument 31-103 – Registration Requirements, Exemptions and Ongoing Registration Obligations (“NI 31-103”). Desmond Kingsford, the principal of the Firm, is registered as the advising representative of the Firm under NI 31-103 with the Commissions.

The information presented in this Letter is not investment advice, should not be relied on as such, and should not be viewed as an investment recommendation by the Firm or Mr. Kingsford generally, or an offer or a solicitation of an offer for the purchase of any securities. Recipients should not make any investment decisions based on the information contained in this Letter. Only (i) an “accredited investor” as defined under section 1.1 of National Instrument 45-106 – Prospectus Exemptions; and (ii) a “permitted client” as defined under section 1.1 of NI 31-103 may invest with the Firm. This Letter is presented solely to illustrate the Firm’s investment process and strategies as of the date indicated on the cover page of this Letter and is based on information provided by management of the Firm as of such date and on beliefs, assumptions, expectations and/or opinions of management as of such date. Certain information contained in this Letter may have been obtained by management of the Firm from third parties and, although believed to be reliable, has not been independently verified and its accuracy, timeliness or completeness cannot be guaranteed.

While the Firm’s investment mandate is designed to reduce risk the program will inherently entail substantial risks. There can be no assurance that the investment objective of the Firm will be achieved. In fact, the investment techniques that the Firm may employ from time to time may, in certain circumstances, substantially increase the adverse impact on the Firm’s investment portfolio. Accordingly, the Firm’s activities could result in substantial losses under certain circumstances. A separately managed account managed by the Firm is highly speculative and there can be no assurance that the investment objectives of the Firm will be achieved. Nothing herein is intended to imply that the Firm’s investment methodologies may be considered “conservative”, “safe”, “risk free” or “risk averse”. Investors must be prepared to bear the risk of a total loss of their invested capital. Past performance of Mr. Kingsford and his affiliates is not necessarily indicative of the future results and any prospective clients of the Firm will need to be prepared to lose all or substantially all of their investment. The Firm will give no warranty as to the performance or profitability of any client account or that the investment objectives of a client’s account will be successfully accomplished.

Certain statements contained in this Letter may be considered “forward-looking information” and “forward-looking statements” (collectively “forward-looking statements”) within the meaning of applicable Canadian securities legislation. All statements, other than statements of historical fact included herein, without limitation, statements relating to the Firm’s future financial performance and investment returns, are forward-looking statements.

Forward-looking statements are frequently, but not always, identified by words such as “expects”, “anticipates”, “believes”, “intends”, “estimates”, “potential”, “possible”, and similar expressions, or statements that events, conditions, or results “will”, “may”, “could”, or “should” occur or be achieved. Forward-looking statements in this Letter include, among other things, statements relating to: the desire to generate outstanding investment results with low risk; the proposed timeline for the Firm’s investment horizon and Mr. Kingsford’s career; the benefits of operating the Firm out of Whistler, British Columbia as opposed to a more traditional investment market; Mr. Kingsford’s beliefs regarding the necessary components to investment success; the future operating or financial performance of the Firm and the assets managed by the Firm; the intention to prioritize long-term investment return over short-term results; the intention to take on more capital only where the Firm believes it will not dilute investor returns; the intention to maintain a fee structure that incentivizes manager performance over asset gathering; the intention to maintain the Firm’s current strategy and vision as it grows; the potential to provide a fund structure in addition to the SMA approach in the future; the Firm’s mission to compound each dollar of invested capital into five dollars over a ten-year period without taking undue risk; the belief that a short term quarterly or annual results focus is harmful to long-term returns; the Firm’s beliefs with respect to how risk is properly defined and mitigated; the Firm’s beliefs as to how returns may actualize; the beliefs of the Firm and Mr. Kingsford regarding the prospective results of specific investments of the Firm; the theories and beliefs disclosed regarding what makes an investment strategy successful; and the expectation and plans for growth . Actual future results may differ materially. There can be no assurance that such statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements reflect the beliefs, opinions and projections on the date of this Letter and are based upon a number of assumptions and estimates that, while considered reasonable by the Firm and Mr. Kingsford, are inherently subject to significant business, economic, competitive, political and social uncertainties, many of which are beyond the control of management. Many factors, both known and unknown, could cause actual results, performance or achievements to be materially different from the results, performance or achievements that are or may be expressed or implied by such forward-looking statements and management of the Firm have made assumptions and estimates based on or related to many of these factors. Readers should not place undue reliance on the forward-looking statements and information contained in this Letter concerning these assumptions.

None of the Firm or Mr. Kingsford or their respective affiliates, associates, shareholders, directors, officers, employees, agents or representatives (collectively, the “Representatives”), as applicable, makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein or any other information (whether communicated in written or oral form) transmitted or made available to recipients, and the Representatives expressly disclaim any and all liability relating to or resulting from the use of this Letter or such other information by a recipient or any of its affiliates, associates or representatives. The Representatives will not be liable for any errors (as a result of negligence or otherwise, to the fullest extent permitted by law in the absence of fraud) in the information, beliefs, assumptions, expectations and/or opinions included in this Letter, or, as noted above, for the consequences of relying on such information, beliefs, assumptions, expectations and/or opinions and further the Representatives disclaim any obligation or undertaking to provide any updates or revisions to any information contained herein to reflect any change in beliefs, opinions, expectations, assumptions or estimates with respect thereto or any change in events, conditions or circumstances on which any statement in this Letter is based.